Modeling a proposed data center tariff: Dominion Energy GS-5

Northern Virginia is the largest data center market in the world, and the largest utility serving it is about to change how it charges the biggest loads on its system. Dominion Energy's GS-5 tariff, designed specifically with data centers in mind, is expected to take effect January 1, 2027.

Under the terms of Dominion's tariff, customers who meet the eligibility criteria for GS-5 will be required to take service on it. That means the question most data center operators are facing isn't whether to move to GS-5, it's what the move means for their cost structure and what contractual commitments they should make within the new tariff. Analyses on contracted demand sizing, site expansion timelines, and long-term budget assumptions all need to happen early enough to inform the capital plans, buildout schedules, and financial forecasts they impact.

To evaluate several scenarios that DC operators need to consider, Arcadia built GS-5 as a custom tariff in Signal using publicly available regulatory filings. We then modeled it on a representative load profile of a 150 MW data center to show what the transition to GS-5 looks like under different operating conditions. Key questions we wanted to understand include:

- How does GS-5 compare to GS-4, the current large load tariff?

- What does GS-5 cost under different operating conditions?

- Which of the structural terms carry the most financial weight?

Our first scenario shows how the GS-4 to GS-5 cost comparison shifts at different utilization levels. The second quantifies what the ramp provision is worth during a phased buildout. Together they demonstrate what becomes possible when the underlying data infrastructure and tariff intelligence exists to model evolving tariffs against the operating conditions specific to each facility, at every site across a portfolio.

The structural commitments in GS-5

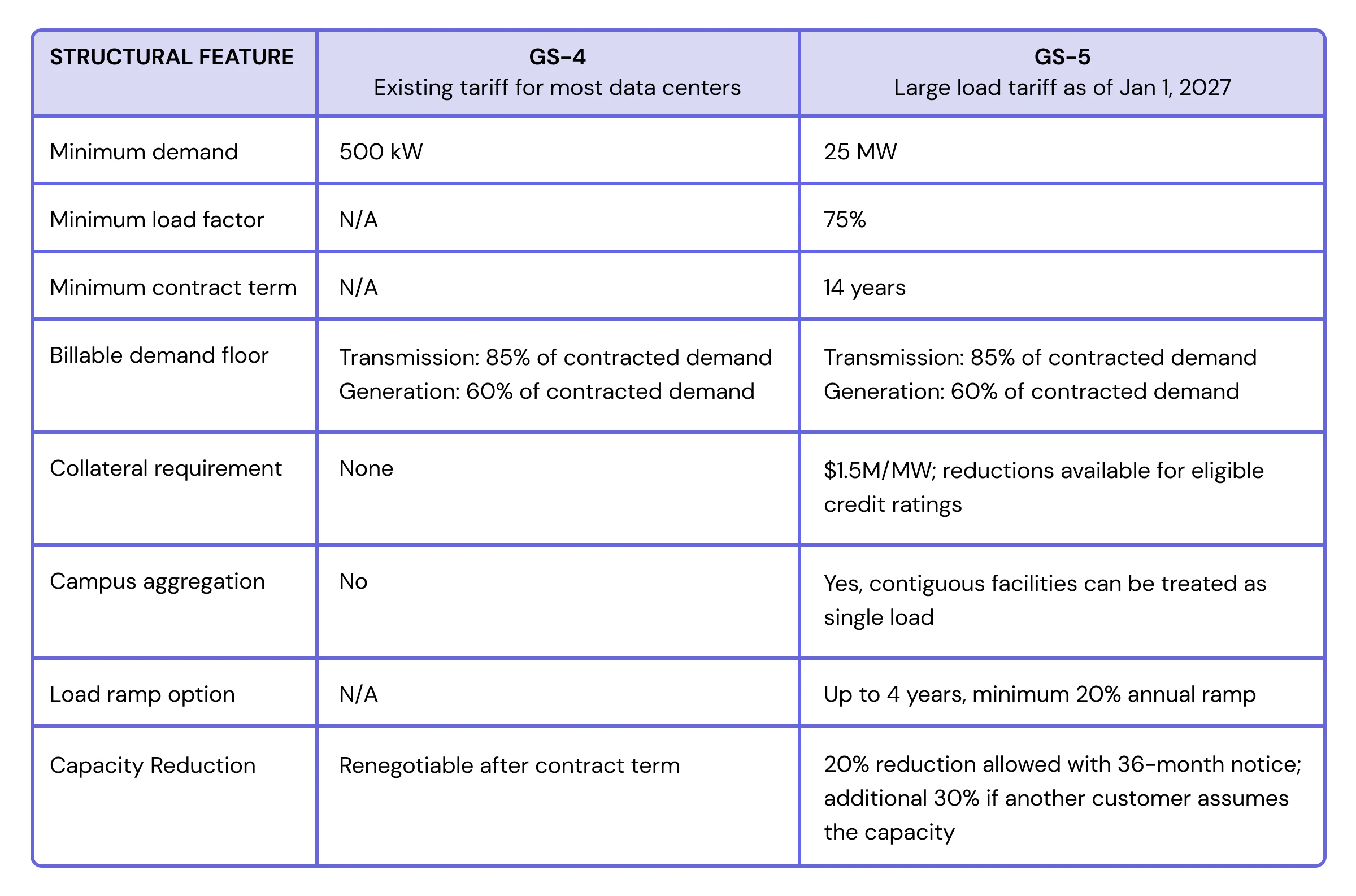

Evaluating GS-5 strictly as a rate change ignores the multi-million dollar risk embedded in its terms. As Dominion Energy deploys capital to support data center load growth, GS-5 serves as their mechanism to ensure long-term cost recovery. By design, the tariff shifts the financial risk of underutilization from utility ratepayers directly to the data center operator. It establishes a 14-year capacity agreement between the load and the utility, where the structural terms matter just as much as the per-unit rates.

The below table compares GS-5 to GS-4, which is the current Dominion Energy tariff that most data centers take service on.

Among the terms of the rate, the 14-year minimum contract and 85% billable demand floor carry the most financial weight if load doesn't perform as planned. A facility running at full utilization absorbs them comfortably. However, a facility that loses a tenant, misses an expansion target, or rebalances workloads carries those terms very differently.

Scenario 1

The Mandatory Transition

Since moving to GS-5 is mandatory for qualifying facilities, operators cannot opt out of its structural terms. Mitigating financial risk starts with accurately sizing contracted demand against actual load. With a strict 85% billing floor, overestimating capacity requirements creates an immediate, unrecoverable cost.

To quantify that exposure – and compare it to business-as-usual under GS-4 – we held contracted demand constant at 150 MW across three scenarios and varied only the facility's actual demand: baseline utilization, a sustained load reduction, and the breakeven point where GS-5 costs are comparable to GS-4.

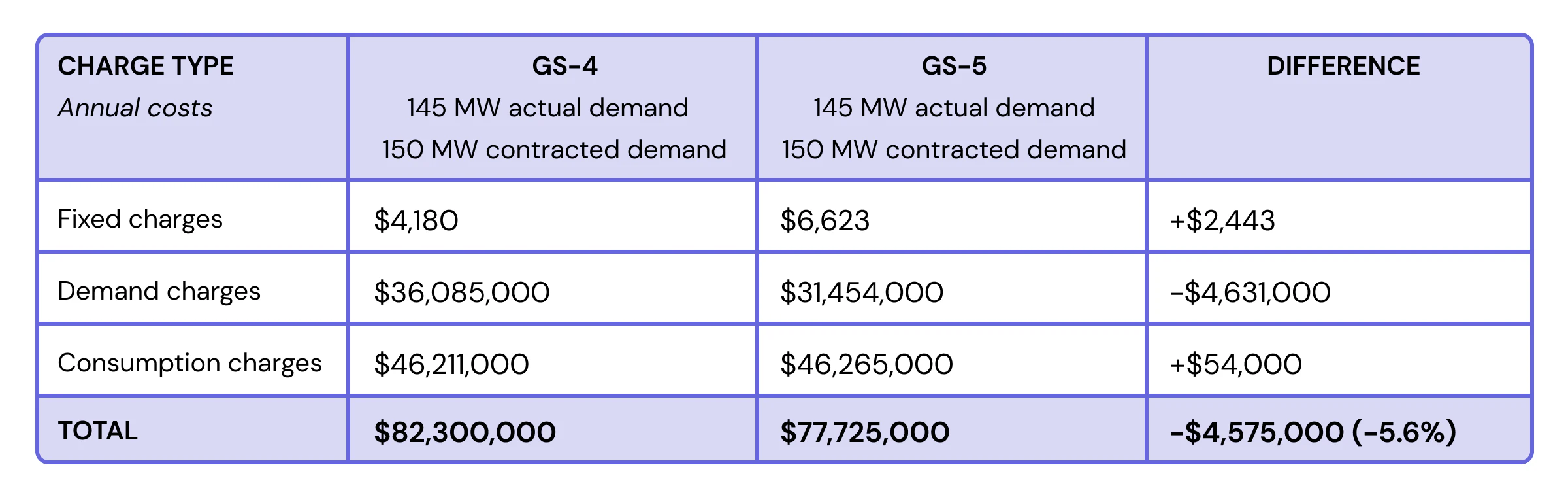

Baseline: Full Utilization

The facility is pulling 145 MW of actual demand against its 150 MW of contracted demand. At this utilization, GS-5 is approximately $4.6 million less per year than GS-4.

The difference is driven almost entirely by demand charges, while consumption costs are nearly identical, and the difference in fixed charges is minimal. For the representative high utilization, high-load-factor facility that we’ve modelled, GS-5's demand charge structure works in the customer's favor.

While the per-unit rates are favorable, the structural terms create a rigid financial floor. The $4.6 million in savings relative to GS-4 only materializes if the facility performs as modeled. To understand where that advantage diminishes, we modeled the tariff against the reality of fluctuating demand.

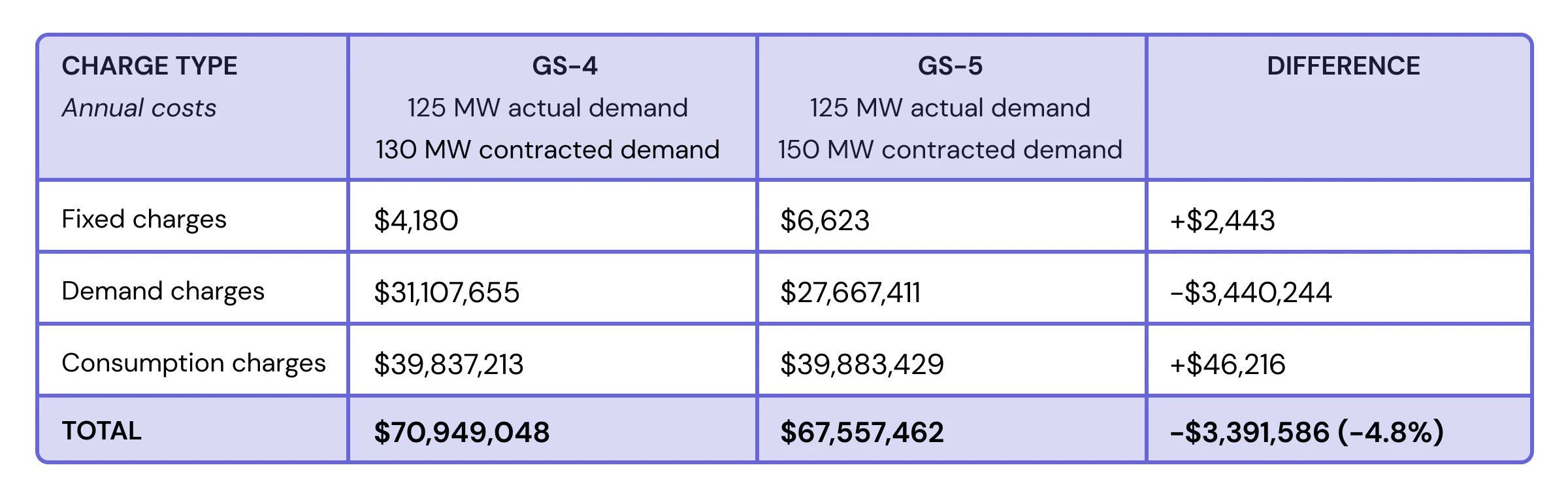

Sustained Load Reduction: Load Drops to 125 MW

A sustained reduction in load alters the cost comparison. On GS-4, a customer whose load drops can re-adjust their contracted demand. On GS-5, that flexibility is replaced by a long-term commitment with very narrow exit ramps: capacity reductions are capped at 20%, require 36 months of notice, and any reduction beyond that requires another qualifying customer to formally assume the released capacity.

When actual demand pulls back to 125 MW, you’ve dropped below the 127.5 MW billing floor. At this point, the savings on GS-5 are neutralized by the cost of capacity you're paying for but not using.

At this level of utilization, the gap between GS-4 and GS-5 narrows from $4.6M to $3.4M. The data center is now being billed against 127.5 MW, the 85% demand floor, despite only drawing 125 MW. That 2.5 MW gap is small now. The scenario below shows how quickly it grows as utilization falls. As utilization continues to drop, the lower unit rates are eventually overtaken by the cost of the 85% billing floor.

Breakeven: How Far Does Demand Have to Fall?

To find the exact breakeven point between GS-4 and GS-5, we modeled where the GS-5 rate advantage evaporates entirely. For a 150 MW contracted demand, this occurs when actual demand falls to approximately 98.6 MW, roughly 66% utilization.

To reach that breakeven, a 150 MW facility would need to lose roughly a third of its load. For most high-utilization operators, the scenario where GS-5 becomes the more expensive rate is unlikely. However, operators should still be aware of downside scenarios, since they are locked into a long-term commitment that remains in force even if business needs shift.

Scenario 2: The ramp decision

Scenario 1 quantified the cost implications for data center operators who are facing a mandatory transition to GS-5, and looking to forecast costs under the new rate relative to their current rate. Scenario 2 shows a different scenario, one where the contracted demand level, not the tariff itself, is the core variable.

For any operator bringing new capacity online, the ramp provision under GS-5 is one of the most consequential elections in the contract. It allows operators to phase in contracted demand over four years, providing a financial buffer as construction phases in or tenants come online, so the billing floor reflects where the facility actually is in its buildout rather than where it's projected to be at full capacity. Instead of paying 85% minimums on the full contract from day one, the floor is calculated on a smaller, stepped base.

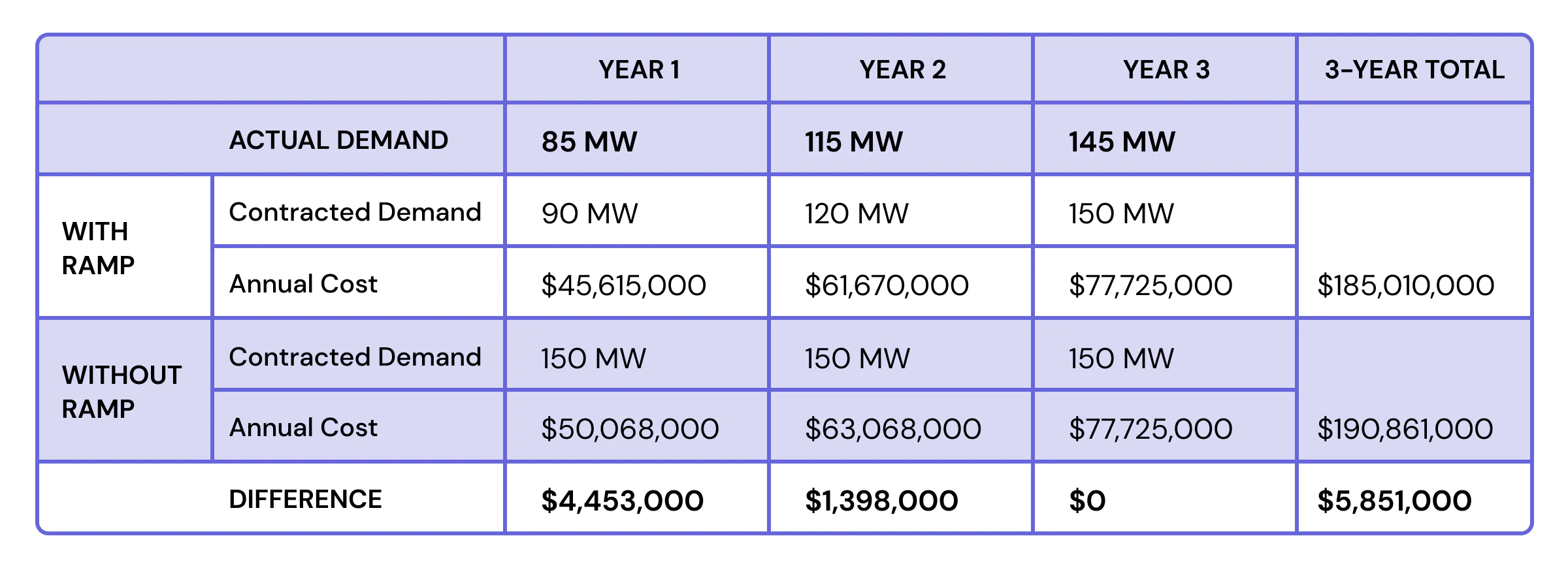

We modeled our representative 150 MW data center taking three years to reach full capacity. One scenario utilizes the ramp; the other locks in the full 150 MW immediately.

Structuring the ramp avoids the cost of a disconnect between your financial commitment and your actual power needs, saving $5.85 million in the first two years. The $5.85 million gap is the cost of a buildout that doesn't go as planned due to forecasting errors, market shifts, or construction delays. An operator who accurately forecasted their ramp and structured their contract accordingly avoids that cost.

What we know about GS-5, so far

The current GS-5 filings reveal four core realities for operators planning ahead:

- Structural terms carry more financial weight than per-unit rates. The 14-year commitment and 85% billing floor determine cost exposure more than the rate itself.

- Contracted demand sizing is the most consequential decision an operator makes before signing. Overestimate, and the billing floor creates an immediate, unrecoverable cost. There's no annual reset.

- The ramp provision is only as useful as the load forecast behind it. Structuring it correctly before signing is one of the few levers operators have to manage contracted demand exposure during a buildout.

- Campus aggregation introduces a separate layer of analysis for operators with contiguous facilities. Whether to aggregate under a single GS-5 contract or have each facility take service independently under GS-4, if the individual loads qualify, is a decision that requires modeling both structures against each site's load profile before signing.

A framework for further evaluation

The above scenarios are a starting point. Decisions about contracted demand levels, ramp structure, load flexibility, and aggregation potential carry multi-million dollar consequences. Understanding which decisions matter most, and by how much, requires running dozens or hundreds of scenarios per site across load profiles, rates, and contractual terms.

GS-5 is one tariff in one market. The same analytical framework applies across an operator’s entire footprint: modeling proposed and revised rates against specific load profiles and contractual structures before decisions are finalized, at every site in a portfolio.

Effectively evaluating an energy strategy at scale requires a partner like Arcadia. Our advisory team works with data center operators to translate tariff mechanics into the financial and operational terms that inform strategic decisions. Through our energy intelligence platform, we combine foundation utility data and energy rate analytics with the speed and scale required to model data center dynamics against ever-changing utility rate structures. With the analytical depth and precision of Arcadia's modeling, data center operators can execute an informed energy strategy that aligns their operations with their long-term financial objectives.

GS-5 rates reflect proposed terms as filed by Dominion Energy in the 2025 biennial review (Case No. PUR-2025-00058) and approved by the Virginia State Corporation Commission. Final rates may be subject to adjustment prior to the January 1, 2027 effective date. GS-4 rates reflect the filing effective January 1, 2026. Arcadia built GS-5 as a custom tariff in Signal using publicly available regulatory filings; scenario inputs were manually configured. The load profile is synthetic and representative.

Optimize your energy management strategy end-to-end. Contact our team to learn more about how Arcadia can support your enterprise energy needs.

Contact us

Join our newsletter

Stay updated with our latest insights, industry trends, and expert tips delivered straight to your inbox